Mutual funds are one of the easiest ways to invest your money and watch it grow. They offer professional management, instant diversification, and the potential for solid returns. But here’s the thing—just investing money and hoping for the best isn’t enough.

To truly maximize your mutual fund returns, you need a smart strategy. In this guide, I’ll share five powerful tips that can help you squeeze every bit of potential from your mutual fund investments and move closer to your financial goals.

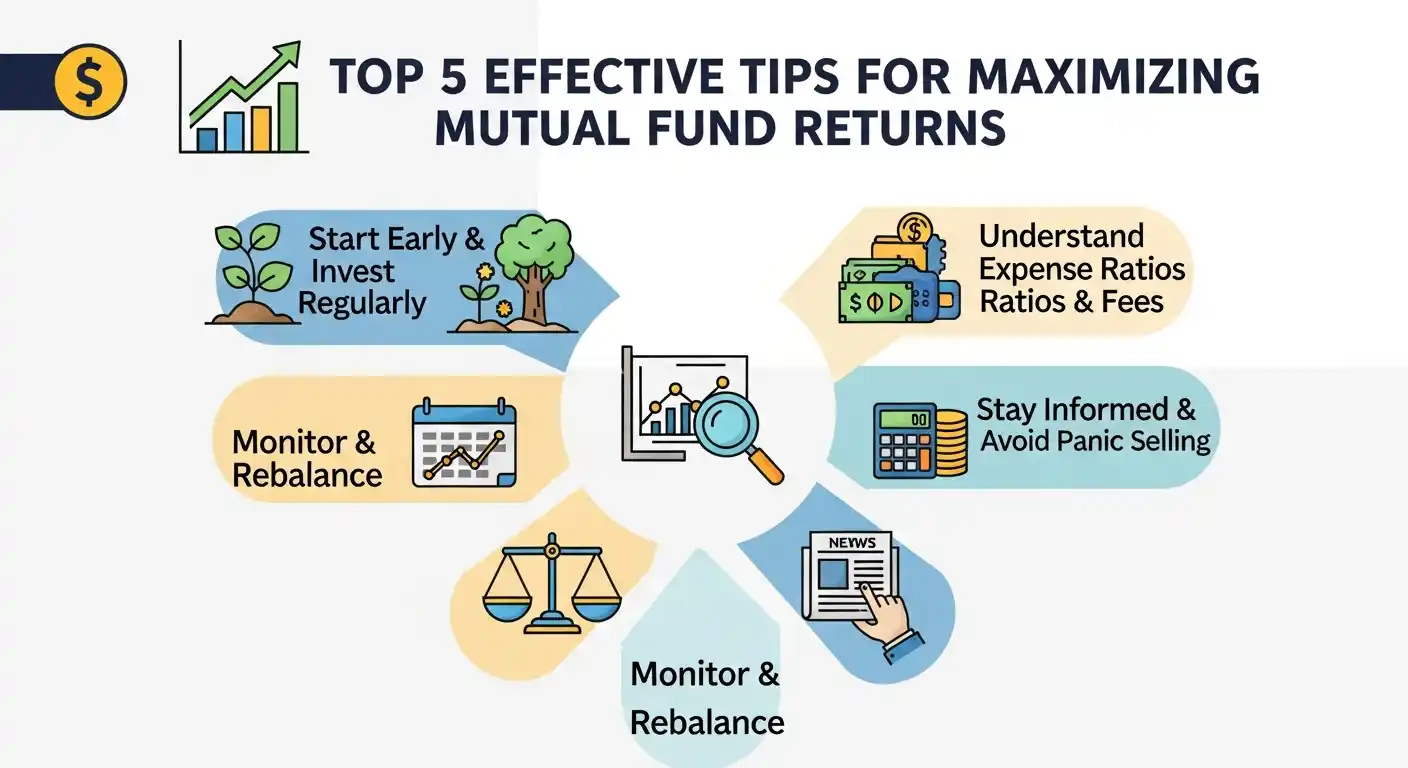

Top 5 Effective Tips for Maximizing Mutual Fund Returns

Let’s dive into practical strategies that actually work.

1. Get Crystal Clear on Your Investment Goals

Before you invest a single rupee, ask yourself: Why am I investing?

This might sound basic, but knowing your “why” changes everything. It helps you pick the right funds and stick with your plan when markets get shaky.

Key Questions to Answer:

What’s your timeline?

- Short-term (1-3 years): Saving for a vacation, wedding, or car? You need safer funds like debt or liquid funds.

- Medium-term (3-5 years): Planning a house down payment? Hybrid or balanced funds work well.

- Long-term (5+ years): Building retirement or education corpus? Equity funds give you the best growth potential.

How much risk can you handle?

- Can’t sleep if your investment drops 10%? Stick to debt funds.

- Okay with ups and downs for better long-term returns? Go for equity funds.

- Somewhere in between? Hybrid funds balance both.

What are you investing for?

- Retirement in 25 years

- Child’s college in 10 years

- Dream home in 5 years

- Tax savings this year (ELSS funds)

Each goal needs a different approach. Match your fund choice to your goal, and you’re already ahead of most investors.

2. Diversify Like a Pro

“Don’t put all your eggs in one basket” isn’t just a saying—it’s your safety net.

Diversification means spreading your money across different types of funds so that if one performs poorly, others can balance it out.

How to Diversify Effectively:

Mix different fund types:

- Equity funds (stocks) – Higher growth, higher risk

- Debt funds (bonds) – Stability and predictable returns

- Hybrid funds – Best of both worlds

- Gold funds – Protection against inflation

Spread across sectors:

Don’t invest everything in banking or IT just because they’re hot right now. What goes up fast can come down just as quickly.

Aim for exposure to:

- Technology

- Banking and Finance

- Healthcare and Pharma

- FMCG (consumer goods)

- Infrastructure and Energy

Example Simple Portfolio:

- 40% Large-cap equity fund (stability)

- 20% Mid-cap equity fund (growth)

- 20% Hybrid fund (balance)

- 15% Debt fund (safety)

- 5% Gold fund (hedge)

This mix protects you when one sector or asset class underperforms while others shine.

3. Review and Rebalance Your Portfolio Regularly

Imagine you start with 60% equity and 40% debt. After a great year in the stock market, your split becomes 75% equity and 25% debt. Now you’re taking more risk than you planned for.

That’s why rebalancing matters.

What is Rebalancing?

It means adjusting your investments back to your original plan by selling some winners and buying more of the laggards.

How to Do It Right:

- Set review dates: Mark your calendar for every 6 months or once a year.

- Check your allocation: Has your 60:40 split become 70:30? Time to rebalance.

- Make adjustments: Sell some equity units and buy debt units to restore your target mix.

- Check fund performance: Is your fund consistently underperforming its benchmark and peers? After giving it 2-3 years, consider switching.

Real-life example:

You invested ₹10 lakhs (₹6L equity, ₹4L debt). After a year:

- Equity grew to ₹8L

- Debt grew to ₹4.2L

- New ratio: 66% equity, 34% debt

To rebalance to 60:40, move ₹70,000 from equity to debt.

This forces you to “sell high and buy low” automatically—the secret to long-term success.

4. Invest Systematically with SIPs

A Systematic Investment Plan (SIP) is like putting your investments on autopilot. You invest a fixed amount every month, regardless of whether the market is up or down.

Why SIPs Work Magic:

Rupee Cost Averaging:

- When markets are low, your ₹5,000 buys more units

- When markets are high, your ₹5,000 buys fewer units

- Over time, your average cost per unit evens out

Power of Compounding:

Regular investments mean your money starts earning returns, and then those returns earn returns. It’s like a snowball rolling downhill—getting bigger as it goes.

Disciplined Investing:

No need to time the market (which is impossible anyway). Just invest every month and let time do the work.

Real-life example:

₹10,000 monthly SIP for 15 years at 12% annual return:

- Total investment: ₹18 lakhs

- Final corpus: Approximately ₹50 lakhs

- Your profit: ₹32 lakhs!

Pro tip: Increase your SIP by 10% every year as your income grows. This “step-up SIP” dramatically boosts your final corpus.

5. Minimize Costs and Fees

Every rupee you pay in fees is a rupee that doesn’t compound for you. Small differences in costs create massive differences over time.

What Costs to Watch:

Expense Ratio:

This is the annual fee charged to manage your fund.

- High expense ratio: 1.5-2%

- Low expense ratio: 0.5-1%

- Index funds: As low as 0.1-0.3%

The impact: A 1% difference in fees can reduce your final corpus by lakhs over 20 years.

Regular vs. Direct Plans:

- Regular plan: Bought through distributor, includes commission (higher expense ratio)

- Direct plan: Buy directly from AMC, no middleman (lower expense ratio)

Always choose direct plans when possible. You can invest through AMC websites or platforms like Groww, Kuvera, or Zerodha Coin.

Exit Loads:

Some funds charge a fee if you exit within 1 year (typically 1%).

- Choose funds with minimal or no exit loads for flexibility

- If a fund has exit loads, understand them before investing

Example:

₹10 lakhs invested for 20 years at 12% returns:

- With 2% expense ratio: ₹72 lakhs

- With 1% expense ratio: ₹89 lakhs

- Difference: ₹17 lakhs!

Small fees make a huge difference.

Bonus Strategies to Supercharge Your Returns

Want to go even further? Here are additional tips to maximize your gains.

Keep Learning and Stay Updated

Markets change, regulations evolve, and new opportunities emerge. Staying informed helps you make better decisions.

How to Stay Sharp:

- Follow reliable financial news (Economic Times, Moneycontrol, Value Research)

- Read mutual fund fact sheets quarterly

- Attend webinars or investment workshops

- Join investment communities online

- Consider consulting a financial advisor for complex decisions

Knowledge is your competitive advantage.

Consider Index Funds for Core Holdings

Index funds simply copy a market index like Nifty 50. They don’t try to beat the market—they just match it.

Why They’re Great:

- Ultra-low fees (0.1-0.5% vs 1.5-2% for active funds)

- Consistent performance (you always get market returns)

- Less volatility than actively managed funds

- No fund manager risk

Smart approach: Use index funds for 30-40% of your portfolio as a stable core, then add active funds for potential outperformance.

Leverage Tax Benefits

Paying less tax means keeping more of your returns.

Tax-Saving Options:

ELSS (Equity Linked Savings Scheme):

- Save up to ₹46,800 in taxes under Section 80C

- 3-year lock-in period (shortest among tax-saving options)

- Potential for equity-like returns

- Kills two birds with one stone: tax savings + wealth creation

Tax-Efficient Holding:

- Hold equity funds for more than 1 year to qualify for long-term capital gains (10% tax on profits above ₹1 lakh)

- Short-term gains (under 1 year) are taxed at 15%

Timing Your Exits:

If you’re close to hitting ₹1 lakh profit in a year, consider spreading your exits across two financial years to minimize tax.

Use Top-Up SIPs

As your income grows, your investments should too.

A top-up SIP lets you automatically increase your investment amount periodically.

Example:

- Start with ₹5,000/month SIP

- Set 10% annual increase

- Year 1: ₹5,000/month

- Year 2: ₹5,500/month

- Year 3: ₹6,050/month

This helps combat inflation and dramatically increases your final corpus.

Reinvest Dividends

If your fund pays dividends, don’t take the cash—reinvest it.

Why? Reinvested dividends buy more units, which earn returns, which compound further. It’s free money working for you.

Most platforms offer “growth” plans that automatically reinvest. Choose those over “dividend” plans.

Common Mistakes That Kill Returns

Avoid these pitfalls:

- Chasing last year’s winners: Just because a fund gave 40% returns last year doesn’t mean it will repeat.

- Panic selling during downturns: Markets recover. Selling during crashes locks in losses.

- Checking portfolio daily: Short-term volatility is normal. Stop obsessing and stay the course.

- Too many funds: More than 8-10 funds becomes unmanageable and creates overlap.

- Ignoring costs: High fees silently eat your returns over time.

- Not having a plan: Random investing without clear goals leads to poor decisions.

Your Action Plan

Ready to maximize your returns? Here’s what to do:

This week:

- Define your financial goals clearly

- Check if you’re in regular plans (switch to direct)

- Review your expense ratios

This month:

- Set up SIPs if you haven’t already

- Check your portfolio diversification

- Mark calendar for quarterly reviews

This year:

- Rebalance your portfolio

- Increase SIPs by 10%

- Consider adding an ELSS for tax savings

Final Thoughts

Maximizing mutual fund returns isn’t about finding magic formulas or timing the market perfectly. It’s about doing simple things consistently well:

- Know your goals

- Diversify smartly

- Review regularly

- Invest through SIPs

- Minimize costs

The real magic happens when you combine these strategies and give them time to work. Start small if needed, but start today. Stay disciplined through market ups and downs. And remember—investing is a marathon, not a sprint.

Your future self will thank you for the smart decisions you make today.

Related Post:

- 10 Tips for Diversifying Your Mutual Fund Portfolio in 2025

- How to Choose Mutual Funds in India in 2025

FAQ on Effective Tips for Maximizing Mutual Fund Returns

How can I determine my investment goals?

List what you’re saving for (retirement, house, education), when you need the money, and how much risk you can handle. This clarity guides every investment decision.

Why is diversification so important?

It spreads risk across different investments so that one poor performer doesn’t sink your entire portfolio. Think of it as financial insurance.

How often should I review my portfolio?

Every 6 months for a quick check, and once a year for detailed review and rebalancing. Don’t check daily—it creates anxiety without adding value.

How can I minimize investment costs?

Choose direct plans over regular plans, prefer index funds for core holdings, avoid funds with high expense ratios (above 1.5%), and be aware of exit loads.

Should I choose actively managed or passive (index) funds?

Use both. Index funds for your core holdings (30-40%) for stability and low costs, and active funds (60-70%) for potential market-beating returns.

How can I stay updated on market trends?

Follow reliable financial news sites, read fund fact sheets quarterly, join investment communities, and consider consulting a financial advisor for major decisions.

What does rebalancing actually do?

It forces you to sell high-performing assets and buy underperforming ones, maintaining your target allocation. This disciplined approach maximizes long-term returns.

Disclaimer: This article is for educational purposes only and not personalized investment advice. Mutual fund investments are subject to market risks. Past performance doesn’t guarantee future results. The strategies mentioned may not suit everyone’s financial situation. Please read all scheme documents carefully and consult a certified financial advisor before making investment decisions based on your specific goals, risk tolerance, and financial circumstances.